by Ariful | Jun 12, 2026 | UK Updates

Understand Your Corporation Tax Rates for 2026

The way you are taxed on your company profits depends on how much you earn. For the 2026 financial year, the tiered system remains the primary way HMRC calculates your liability. Understanding where you fall within these bands will help you forecast your cash flow more accurately.

- The Small Profits Rate (19%): If your company’s augmented profits are £50,000 or less, you will typically pay the 19% rate. This is designed to support smaller businesses and start-ups as they find their footing.

- The Main Rate (25%): If your profits exceed £250,000, your company will be subject to the 25% main rate.

- Marginal Relief: If your profits fall between £50,000 and £250,000, you don’t jump straight to 25% on everything. Instead, you pay a gradually increasing effective rate. This ensures there isn’t a “tax cliff” as your business scales.

Keep in mind: If you have associated companies (other companies under the same control), these thresholds are divided between them. We recommend keeping a close eye on your group structure to avoid unexpected tax hikes.

Monitor the £90,000 VAT Registration Threshold

VAT compliance is often the most complex area for digital businesses and ecommerce sellers. As of 2026, the VAT registration threshold remains at £90,000 of taxable turnover in any rolling 12-month period.

Register early to avoid retrospective fines. If you expect your turnover to cross this limit within the next 30 days, or if you have already crossed it in the last 12 months, you must register. Once registered, you are required to charge VAT on your sales and, crucially, you can reclaim VAT on your business-related purchases.

Doing this properly will save you significant amounts of money on stock and digital services, but it does require strict record-keeping. Under the current Making Tax Digital (MTD) rules, all VAT-registered businesses must use compatible software to file their returns. This is where a structured tax accounting service becomes essential to ensure every transaction is captured accurately.

Simplify Your Payroll and Director’s Salary

As a director of a UK Limited Company, you are also an employee. This means you need to set up a Pay As You Earn (PAYE) scheme with HMRC. Even if you are the only person in the company, maintaining a payroll system is essential for taking a salary and making National Insurance contributions.

Most directors choose a “low salary, high dividend” strategy to remain tax-efficient. However, even a small salary requires regular Real-Time Information (RTI) submissions to HMRC. Submit these on time to avoid automatic late-filing penalties. By managing this correctly, you ensure you are building up your qualifying years for the State Pension while keeping your company’s tax bill as low as possible.

Prepare for Making Tax Digital (MTD) Updates

2026 marks a major turning point for HMRC’s digital roadmap. While Limited Companies already use digital systems for VAT and Corporation Tax filings, a new phase of Making Tax Digital for Income Tax begins on April 6, 2026.

If you are a business owner who also receives significant income from sole trader activities or other sources outside your Limited Company (totalling over £50,000), you will need to comply with new quarterly reporting requirements for your personal tax return. Don’t worry, this doesn’t change how your Limited Company files its accounts, but it does mean your personal tax affairs will require more frequent attention.

Maintain Accurate Records with a Structured System

The secret to stress-free tax compliance is ongoing bookkeeping. Gone are the days of handing a box of receipts to an accountant once a year. To succeed in 2026, you need a tech-driven approach that captures data daily.

It is essential to use cloud-based software to track your income and expenses. This allows you to:

- See your real-time tax liability so you aren’t surprised by a bill at year-end.

- Reconcile bank statements instantly to ensure no expenses are missed.

- Store digital copies of receipts, fulfilling HMRC’s requirements for digital record-keeping.

Our team handles the daily bookkeeping, VAT filings, and year-end accounts, so you can focus on scaling your brand.

Take Control of Your Compliance Today

HMRC compliance doesn’t have to be a hurdle. With the right structure and a partner that understands the nuances of UK Limited Companies and cross-border trade, you can navigate these rules with confidence.

Whether you are an ecommerce seller moving goods into Europe or a digital agency based in the UK, we are here to ensure your filings are accurate and your deadlines are met. Let us handle the complexity while you build your business.

Contact us today to discuss how our Full Compliance Suite can streamline your business in 2026.

Frequently Asked Questions

What is the Corporation Tax deadline for UK Limited Companies?

Your Corporation Tax payment is usually due 9 months and 1 day after the end of your accounting period. Your Company Tax Return (CT600) is due 12 months after the end of your accounting period.

Do I need to register for VAT if I sell to customers outside the UK?

This depends on where your customers are located and where your goods are held. For many international sellers, VAT registration is required even before the £90,000 threshold is met. We specialise in cross-border VAT and can help you determine your exact requirements.

Can I file my own accounts to HMRC?

Yes, you can, but it is highly risky for growing businesses. HMRC’s rules for iXBRL tagging and digital submissions are strict. Errors can lead to audits and heavy fines. Using a structured compliance service ensures your accounts are filed correctly every time.

What happens if I miss a tax deadline?

HMRC issues automatic penalties for late filings and late payments. These start small but can escalate quickly to hundreds or thousands of pounds. Staying ahead of deadlines is the easiest way to protect your company’s profits.

by Ariful | Jun 11, 2026 | UK Updates

Expanding Your UK Limited Company into the USA, Canada, and Australia

Expanding your UK Limited Company into the USA, Canada, and Australia is a landmark achievement. It represents growth, brand maturity, and a massive increase in your potential customer base. However, for many UK business owners, the excitement of “going global” is quickly dampened by the realization that compliance isn’t a one-size-fits-all process.

If you treat international tax as a series of disconnected tasks, you risk falling into a trap of missed deadlines, double taxation, and expensive penalties. In 2026, the regulatory landscape is more interconnected than ever. Tax authorities now share data across borders to identify non-compliant sellers. To thrive, you need more than just an accountant; you need a unified compliance strategy.

At Sterlinx Global, we operate as your Global Tax Compliance Suite. This means you provide the data, and we handle the end-to-end delivery of bookkeeping, tax calculations, and filings across these major jurisdictions.

Navigate the Complex Maze of US Sales Tax Nexus

The United States is often the first stop for UK exporters, but it is also the most complex. Unlike the UK’s flat VAT system, the US has no federal sales tax. Instead, you must deal with over 11,000 different tax jurisdictions across 50 states.

The biggest hurdle for UK sellers is the concept of Nexus. This is the legal “connection” your business has with a state that requires you to collect and remit sales tax.

- Economic Nexus: Following the 2018 Wayfair ruling, you no longer need a physical office or warehouse to be liable for tax. In 2026, most states enforce a threshold (typically $100,000 in sales or 200 transactions). Once you cross this line, you must register.

- Physical Nexus: If you use Amazon FBA or a third-party logistics (3PL) provider in the US, you likely have physical nexus in those states immediately. Storing even a single unit of inventory can trigger registration requirements.

- Federal Reporting for LLCs: If you have established a USA LLC to support your UK operations, you face strict IRS reporting. Form 5472 is a critical requirement for foreign-owned LLCs. Missing this filing can result in a minimum penalty of $25,000.

Action Item: Conduct a nexus review at least once a quarter. Map your sales by state to ensure you aren’t quietly slipping over thresholds without realizing it.

Master the Canadian GST/HST and Provincial Rules

Canada offers a lucrative market, but its tax system is a hybrid of federal and provincial rules. For a UK business, understanding the difference between GST, HST, and PST is essential for maintaining your profit margins.

- GST/HST Registration: Most non-resident businesses must register for the Goods and Services Tax (GST) or Harmonized Sales Tax (HST) once their worldwide taxable supplies in Canada exceed CAD 30,000 over four consecutive quarters.

- The “Carrying on Business” Test: Canada uses a fact-based test to determine if you are “carrying on business” in the country. This can include having inventory in a Canadian warehouse or even just targeting Canadian consumers through local marketing.

- Provincial Sales Tax (PST): Provinces like British Columbia, Saskatchewan, and Manitoba have their own sales tax systems separate from the federal GST. If you sell into these regions, you may need separate provincial registrations.

Don’t worry, while the terminology is different from the UK, the logic is similar. By integrating your Canadian sales data into a unified accounting system, you can ensure that you are charging the correct rate (which varies from 5% to 15%) depending on the customer’s province.

Simplify Your Australian GST Obligations

Australia has streamlined its system for international sellers, but the Australian Taxation Office (ATO) is vigilant about enforcement. As a UK brand, you are likely subject to Australian GST if your sales “connected with Australia” exceed AUD 75,000 annually.

- Low-Value Goods Regime: If you sell physical goods valued at AUD 1,000 or less directly to Australian consumers, you are responsible for collecting and remitting 10% GST.

- Simplified vs. Full Registration: For many UK businesses, a “Simplified GST” registration is the best path. It allows you to report and pay GST without needing an Australian Business Number (ABN), though it does not allow you to claim GST credits on local purchases.

- 2026 Transparency Rules: Be aware that Australia has increased its focus on large multinational groups. If your global revenue is significant, you may face additional reporting requirements regarding your tax strategy and presence.

To stay ahead, ensure your e-commerce platform (Amazon, Shopify, or eBay) is correctly configured to identify Australian customers and apply the 10% GST at the point of sale.

Why a Unified Strategy is Non-Negotiable

Trying to manage US Sales Tax, Canadian HST, and Australian GST using three different local accountants and five different spreadsheets is a recipe for disaster. This fragmented approach often leads to “data silos,” where your bookkeeping doesn’t match your tax filings, or worse, you end up paying tax twice on the same transaction.

A unified strategy provides three major benefits:

- Consistent Reporting: When one partner handles your global compliance, your UK year-end accounts will perfectly reflect your international tax liabilities. This is essential for accurate tax accounting and financial planning.

- Reduced Overhead: Instead of paying multiple sets of “onboarding” fees and dealing with different time zones, you have a single point of contact who understands your entire global footprint.

- Proactive Risk Management: Tax laws change. In 2026, we are seeing rapid updates to digital service taxes and threshold adjustments. A unified partner can spot a potential nexus trigger in the US before it becomes a legal problem, or advise you on how a change in Australian law affects your Canadian supply chain.

How Sterlinx Global Delivers Compliance

We don’t just provide advice; we deliver compliance. Our model is built for the modern, fast-growing SME. We specialize in taking the raw data from your marketplaces and digital platforms and turning it into accurate, filed returns.

Our Service Matrix covers:

- UK & Ireland: Full-suite accounting, VAT, bookkeeping, and year-end filings.

- USA, Canada, & Australia: Comprehensive tax registrations, sales tax/GST/HST calculations, and ongoing compliance filings.

- European Union: VAT registration and filings across major jurisdictions like Germany, France, and Spain.

We operate as an extension of your team. You focus on scaling your brand and finding new customers; we ensure that every dollar, pound, and loonie you earn is accounted for and compliant with local laws.

Secure Your Global Growth Today

The most successful UK businesses are those that see compliance as a foundation for growth rather than a hurdle to be cleared. By centralizing your USA, Canada, and Australia compliance, you protect your business from the “hidden costs” of international expansion, fines, audits, and reputational damage.

by Ariful | Jun 10, 2026 | European VAT

Scaling Your E-Commerce Business Across International Borders

Scaling your e-commerce or digital business across international borders is a significant milestone. However, the complexity of cross border VAT can often feel like a barrier to your global ambitions. Whether you are selling physical goods from a UK hub to Europe or managing a digital agency with clients in the USA and Canada, staying compliant is non-negotiable.

In this strategy session, we break down the essentials of international tax compliance. We will look at why professional vat return services uk are your best tool for expansion and how to prepare for the critical regulatory shifts arriving in July 2026.

The 3-Minute Cheat Sheet: UK and EU Rules

If you only have three minutes, here is the essential framework for cross-border compliance in 2026.

1. Selling into the UK

If your business is based outside the UK but you are selling to UK customers, you must understand the “First Sale” rule. Unlike UK-based businesses that enjoy an £85,000 registration threshold, non-established taxable persons (NETPs) must generally register for UK VAT as soon as they make their first taxable sale.

- Consignments under £135: You must collect UK VAT at the point of sale (your checkout) and report it via your UK VAT return.

- Consignments over £135: Import VAT and customs duties are typically due at the border, though demystifying postponed vat accounting can significantly improve your cash flow by allowing you to declare and recover import VAT on the same return.

2. Selling into the EU

The European Union uses a “Destination Principle,” meaning VAT is usually due where your customer lives.

- The €10,000 Threshold: This only applies to EU-established businesses. If you are a non-EU seller, you are liable for VAT from your very first sale.

- IOSS (Import One-Stop Shop): For consignments under €150, IOSS allows you to collect VAT at checkout, facilitating faster customs clearance and a better customer experience.

- OSS (One-Stop Shop): If you hold stock in one EU country (like Germany) and ship to consumers in another (like France), the One-Stop Shop procedure allows you to file a single return for all intra-EU B2C sales.

New for July 2026: The €3 EU Customs Shift

A major change is approaching on July 1, 2026. Historically, parcels valued under €150 were exempt from customs duties (though still subject to VAT). The EU is removing this relief.

From next month, a flat €3 customs duty per item will apply to low-value e-commerce parcels imported from non-EU countries. This is an interim measure as part of a broader customs reform. If you use IOSS, your VAT handling remains simplified, but you must factor this new duty into your pricing strategy or shipping terms to avoid “sticker shock” for your customers at the doorstep.

Why Professional VAT Return Services UK are Critical

Managing VAT is not just about calculations; it is about operational execution. When you trade across borders, your data comes from multiple sources: Amazon, Shopify, eBay, and your payment gateways.

At Sterlinx Global, we operate as a Global Tax Compliance Suite. We don’t just advise you on what to do; we handle the day-to-day compliance. Our systems integrate directly with your platforms, for instance, helping you incorporate Shopify VAT reports seamlessly to ensure every penny is accounted for and filed correctly with HMRC or EU tax authorities.

Using professional vat return services uk ensures:

- Accuracy: We reconcile your sales data against your bank records daily.

- Deadlines: Never miss a filing date, avoiding costly late-payment penalties.

- Consistency: Whether you are dealing with UK VAT, German VAT, or Spanish filings, your compliance is managed in one central location.

Your Weekly Strategy Checklist

To keep your cross-border operations running smoothly, incorporate these steps into your weekly management routine:

Monday: Data Reconciliation

Review your sales reports from the previous week. Check that your checkout systems are applying the correct VAT rates based on the customer’s location. If you have recently expanded into a new territory, verify that your OSS reporting is capturing those sales accurately.

Wednesday: Inventory and Threshold Monitoring

Monitor where your stock is held. If you use Amazon FBA and your goods are moved to a warehouse in a new country, this often triggers an immediate VAT registration requirement in that jurisdiction. Keep a close eye on your “distance selling” volumes to ensure you aren’t nearing any new liability points.

Friday: Compliance Audit

Ensure all your import documentation (C79 certificates or PVA statements in the UK) is organized. If you are importing goods, verify that your IOSS number is correctly formatted on shipping labels. Small errors here lead to parcels being held at customs, resulting in negative customer reviews and increased support costs.

Managing the Logistics of Cross Border VAT

One of the biggest challenges in cross border vat is the sheer volume of transactions. If you are a high-volume seller, manual spreadsheets are no longer viable. You need a structured, tech-driven system that provides real-time visibility into your tax liabilities.

We specialise in helping digital businesses and SMEs bridge the gap between their sales platforms and tax authorities. Whether you need to navigate WooCommerce VAT returns or manage complex Amazon FBA filings across five European countries, our team ensures the data flows correctly.

The Sterlinx Service Matrix

We provide a flexible, modular approach to your global expansion:

- Full Compliance Suite: Available for the UK, Ireland, USA, Canada, and Australia. This covers everything from bookkeeping to year-end accounts.

- VAT-Only Services: Specifically for the European Union. We handle your VAT registrations and filings in key markets like Germany, France, Italy, Spain, and the Netherlands.

Common Pitfalls to Avoid in 2026

- Ignoring the €3 Flat Duty: Don’t wait until July 1 to adjust your pricing. Analyze your margins now to see how the new EU customs fee impacts your profitability on low-value items.

- Assuming “Digital” Means “Tax-Free”: Many SaaS and digital service providers mistakenly believe they don’t need to worry about VAT. In reality, digital services are taxed where the customer is located. If you have customers in the EU, you likely need a Non-Union OSS registration.

- Delayed Registration: Waiting until you hit a threshold (or realizing too late that you didn’t have one) can lead to backdated tax bills and heavy fines. It is always better to contact us early to map out your registration roadmap.

Final Thoughts: Growth Through Compliance

Cross border VAT should be viewed as a cost of doing business in a global market. The right professional guidance and systems can transform it from a burden into a competitive advantage. By staying ahead of regulatory changes and maintaining clean, accurate records, you free up mental energy to focus on what you do best: growing your business.

by Ariful | Jun 9, 2026 | UK Accounting

Running a UK Limited Company is an exciting journey, but the transition from a “great idea” to a “compliant business” often comes with a steep learning curve. When it comes to uk limited company accounting, the margin for error is smaller than most business owners realise.

Small mistakes in your bookkeeping or filing can quickly snowball into hefty HMRC fines, interest charges, and a lot of unnecessary stress. Whether you are an ecommerce seller, a digital agency, or a growing SME, staying on top of your numbers is the only way to ensure your business survives and thrives.

Don’t worry; most of these errors are easily fixable if you catch them early. Here are the seven most common accounting mistakes UK business owners make and exactly how you can avoid them.

1. Mixing Personal and Business Finances

This is the most common mistake for new directors. When you operate as a sole trader, the “business money” is essentially “your money.” However, a Limited Company is a separate legal entity. The moment you start using your business account to buy groceries or your personal card to pay for software, you create a bookkeeping nightmare.

Why this hurts you:

- Audit Risk: HMRC looks unfavourably on messy records.

- Wasted Time: You (or your accountant) will spend hours unpicking which transactions are business-related.

- Tax Inefficiency: You might miss out on legitimate business expenses because they are buried in your personal bank statement.

The Fix: Open a dedicated business bank account immediately. If you’re still using high-street banks and find them too slow, you might want to look into fintech options for UK SMEs. Never “borrow” money from the company without recording it as a dividend or a director’s loan.

2. Missing Companies House Deadlines

Many business owners focus solely on HMRC and forget about Companies House. As a director, you have two primary filing obligations here: your Annual Accounts and your Confirmation Statement (CS01).

In 2026, the rules around identity verification for directors have tightened, and the fees for filing have increased. For example, the digital confirmation statement fee is now £50.

The Consequences:

- Automatic Fines: Filing your accounts even one day late results in an automatic £150 fine, which doubles if you’re more than three months late.

- Strike-off Action: If you consistently ignore your Confirmation Statement, Companies House can assume the company is no longer trading and begin the process of striking it off the register.

The Fix: Set digital reminders for your “Accounting Reference Date.” Better yet, use a structured system where your accounting services for small business uk handle these filings on your behalf automatically.

3. Ignoring the £90,000 VAT Threshold

In the UK, the VAT registration threshold is currently £90,000. The mistake many sellers make is thinking this is based on a fixed tax year (April to April). It isn’t. It is based on a rolling 12-month period.

The Risk:

If your taxable turnover for the last 12 months exceeds £90,000 today, you must register for VAT. If you realise six months late that you crossed the threshold, HMRC will backdate your registration. You will be liable for the VAT on all sales made since that date: even if you didn’t charge your customers VAT at the time.

The Fix: Monitor your rolling 12-month turnover at the end of every single month. If you are an ecommerce seller, this is even more critical as cross-border rules can complicate your VAT position. Stay updated with the latest HMRC VAT insights for 2026 to ensure you aren’t caught out.

4. Failing to Set Aside Money for Tax

Profit is not the same as cash in the bank. Many directors see a healthy balance at the end of the month and spend it on growth or dividends, only to be shocked by a massive Corporation Tax or VAT bill six months later.

In 2026, Corporation Tax rates remain a significant consideration for profitable companies. Additionally, dividend tax rates have increased, meaning your personal tax liability as a director might be higher than you expected.

How to Stay Safe:

- VAT: Set aside 20% of every sale (or your specific VAT rate) into a separate “Tax Savings” account.

- Corporation Tax: Estimate your profit and set aside roughly 19-25% of it every month.

- PAYE/NIC: If you have employees, remember that the money you deduct from their wages belongs to HMRC, not you.

The Fix: Update your bookkeeping weekly. Seeing your “Estimated Tax Liability” in real-time allows you to make informed decisions about whether you can actually afford that new hire or office upgrade.

5. Poor Record Keeping and MTD Non-Compliance

Making Tax Digital (MTD) is no longer a “future plan”: it is the law for VAT-registered businesses and is expanding to other areas of tax. Storing receipts in a shoebox or managing your accounts on a complex, manual spreadsheet is a recipe for disaster.

The Problem:

- Inaccurate Data: Manual entry leads to typos.

- Lost Expenses: If you lose a receipt, you lose the ability to claim that tax relief.

- HMRC Penalties: Under MTD, you must keep “digital records” and use “functional compatible software” to submit your returns.

The Fix: Move to a cloud-based accounting system. Use apps to snap photos of receipts the moment you receive them. Digital record-keeping isn’t just about compliance; it gives you a clear window into your business performance. If you’re struggling with the transition, our 2026 tax refresh guide provides a roadmap for modern SME support.

6. Mishandling the Director’s Loan Account (DLA)

The Director’s Loan Account is a record of the transactions between you and your company. A common mistake is letting this account become “overdrawn”: meaning you owe the company money.

The Tax Trap:

If your DLA is overdrawn by more than £10,000 at any point, it can be treated as a “benefit in kind,” which triggers personal tax. Furthermore, if the loan isn’t paid back within nine months of your year-end, the company has to pay a special tax called “S455 tax” at 33.75%.

The Fix: Always record whether a withdrawal is a salary payment, a dividend, or a loan repayment. Keep your DLA reconciled and aim to clear any overdrawn balance before the year-end deadline to avoid unnecessary tax charges.

7. The “DIY” Debt: Waiting Too Long for Professional Support

Many small business owners try to save money by doing everything themselves. While “DIY” accounting might work when you have three invoices a month, it quickly becomes a liability as you scale.

The time you spend trying to figure out VAT codes or reconciling Amazon settlements is time you aren’t spending on sales, marketing, and product development.

by Ariful | Jun 8, 2026 | Banking

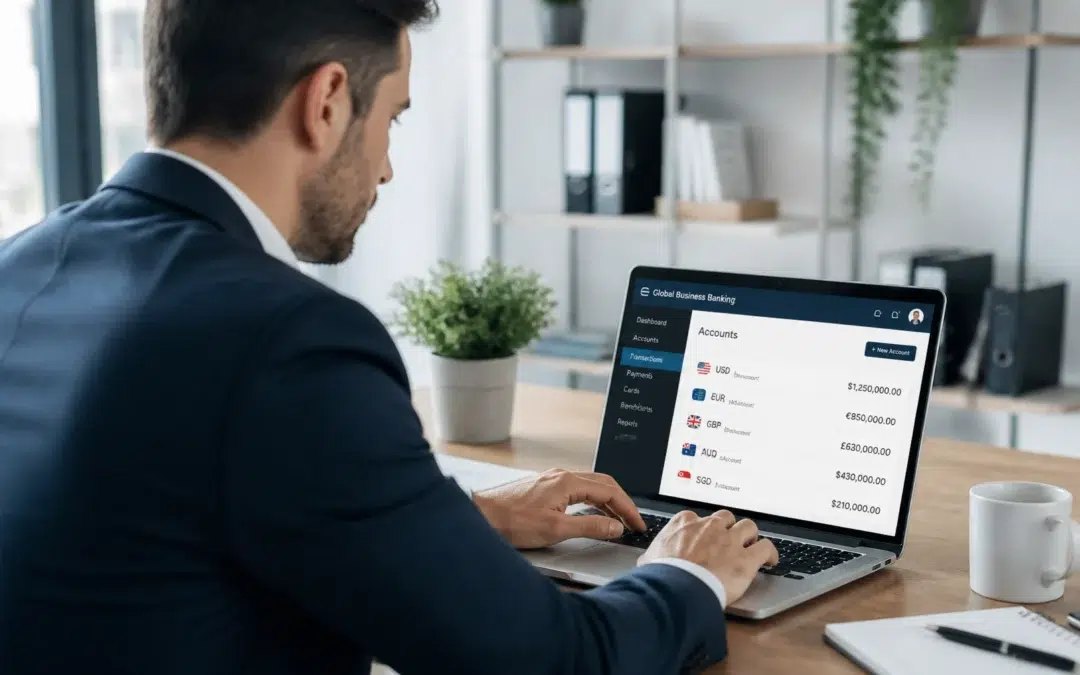

Managing Global Banking for UK Limited Companies in 2026

Managing finances for a UK Limited Company used to be simple: you opened a high-street bank account, and that was it. But in 2026, if you are trading across borders, selling on Amazon US, hiring contractors in Europe, or running a Shopify store for Australian customers, your banking needs have evolved.

The gap between “traditional banking” and “global commerce reality” is where many SMEs lose thousands in hidden fees and compliance errors. At Sterlinx Global, we see these patterns every day. We don’t just handle your tax filings; we see the data behind the transactions.

If you want to protect your margins and stay compliant, stop making these seven common global banking mistakes.

1. Paying the “Loyalty Tax” to High-Street Banks

Many SMEs stick with their domestic bank for international trade simply because it’s familiar. This is a costly mistake. Traditional banks often charge excessive SWIFT fees and apply an “FX spread” (the difference between the market rate and what they give you) of up to 3-5%.

The Fix: Switch to a Multi-Currency Fintech Solution

Modern platforms allow you to hold, receive, and send money in dozens of currencies at near-market rates. By using a specialist multi-currency account, you can save enough in FX fees to cover your entire monthly accounting bill. For a deeper dive, check out our guide on how to choose the best multi-currency business account.

2. Treating Foreign Exchange (FX) as an Afterthought

Are you simply “accepting the rate of the day” when you pay a supplier in China or receive USD from a US customer? If so, you are gambling with your profit margins. A 2% shift in currency value can wipe out the profit on an entire shipment.

The Fix: Implement a Natural Hedging Strategy

Don’t convert currency unless you have to. If you receive USD from sales, keep it in a USD pocket of your multi-currency account. Use that same USD to pay your US-based software subscriptions or suppliers. This is called “natural hedging,” and it eliminates conversion costs entirely.

3. The Reconciliation Nightmare: Manual Data Entry

If you are still manually downloading CSV files from your bank and uploading them to your accounting software, you are inviting human error. Manual reconciliation is the leading cause of “ghost” expenses and missed tax deductions.

The Fix: Enable Direct API Bank Feeds

Ensure your banking provider has a direct integration with your accounting platform. This allows transactions to flow into your books in real-time. At Sterlinx Global, we integrate your bank feeds directly into our compliance suite, ensuring your UK Limited Company accounting is always accurate and up-to-date without you lifting a finger.

4. Ignoring Local Payment Rails

Relying solely on the SWIFT network for every international payment is slow and expensive. SWIFT payments often pass through “intermediary banks,” each of which takes a small cut of your money before it reaches the destination.

The Fix: Use Local IBANs and Account Details

A high-quality global banking partner will provide you with local account details for the UK (Sort Code/Account Number), USA (ACH Routing), and Europe (SEPA IBAN). This allows you to receive money as if you had a local physical presence, making it faster for your customers and cheaper for you.

5. Neglecting Multi-Entity Compliance and KYC

Opening a foreign account is easy; keeping it open is the hard part. Many SMEs fail to provide the correct “Know Your Customer” (KYC) documentation or fail to disclose their full ownership structure, leading to frozen accounts during critical sales periods.

The Fix: Maintain a “Compliance Folder”

Keep your Certificates of Incorporation, shareholder registers, and Proof of Address documents updated and ready to go. Remember, global banking is inextricably linked to tax compliance. If you are trading in the USA, Canada, or Australia, ensure your entity structure is optimized for both banking and tax. Our Ultimate Guide to Cross-Border Compliance covers exactly what you need to stay in the green.

6. Falling for “Ghost” Fees and Hidden Spreads

Some providers advertise “zero-fee” transfers but hide their profit in a heavily marked-up exchange rate. If you aren’t checking the “all-in” cost of a transaction, you are likely overpaying.

The Fix: Calculate the Total Cost Per Transaction

Before sending a large transfer, compare the rate offered by your bank against the “Mid-Market Rate” (found on Google or Reuters). The difference is your real cost. Aim for a provider that offers transparent pricing and low fixed fees rather than hidden percentages.

7. Weak Cybersecurity and Shared Logins

In the rush to scale, many SMEs share a single set of banking credentials among three different staff members. This is a massive security risk and a compliance red flag. If a fraudulent transaction occurs, you will have no “audit trail” to prove who authorized it.

The Fix: Enforce Role-Based Access and MFA

Never share passwords. Use a banking platform that allows you to invite team members with specific roles (e.g., a “viewer” role for your accountant and an “approver” role for the director). Always enable Multi-Factor Authentication (MFA) via an app like Google Authenticator, not just SMS.

Why Compliance is Your Secret Banking Weapon

Managing global banking isn’t just about moving money; it’s about the data that lives behind that money. Every transaction you make impacts your VAT filings, your year-end accounts, and your corporation tax liability.

At Sterlinx Global, we operate as your Global Tax Compliance Suite. We don’t just tell you what happened last month; we provide an ongoing, tech-driven system that handles your bookkeeping, VAT/GST filings, and financial reporting daily. When your banking and your accounting work in harmony, you stop worrying about deadlines and start focusing on growth.

Stop guessing and start scaling. If you need a structured, reliable partner to handle the complexities of cross-border compliance and accounting, we are here to help.

Contact us today to see how we can streamline your global operations.

Frequently Asked Questions

Can I use a UK business account for US Amazon sales?

You can, but you shouldn’t. Amazon will convert your USD sales into GBP at a poor exchange rate (often 3-4% loss). It is much better to use a multi-currency account with US routing details to receive USD directly.

What is the difference between a traditional bank and a fintech “neo-bank”?

Traditional banks offer physical branches and credit products but are often slow and expensive for international transfers. Fintechs are digital-first, offering faster setup, better apps, and significantly lower FX costs.

Do I need a separate bank account for every country I sell in?

No. A single multi-currency account from a provider like Payoneer, Airwallex, or Wise can provide you with local account details for multiple countries without opening separate accounts.